From Renting to Owning: How I Paid Off a $171,278 Property in 3 Years

Are you sick of paying astronomical rent and wishing you had a place of your own?

Rent has been rising, and it's getting harder and harder to buy a house.

Everyone wants to purchase a home in order to survive this unpredictable recession and the current market situation. On top of that, the recent bank closures and high interest rates make it appear nearly impossible for anyone to get a mortgage loan from a bank.

I know how you feel because I was in the same exact situation in 2020.

I was fed up with paying rent every month, knowing that I was helping pay someone else’s mortgage! And, in reality, it could be so much better to own my own place. So I decided to start navigating the challenging terrain of purchasing a home and take control of my future.

My journey began with a goal: get a home in less than three years. I knew it would be tremendously challenging, but I was determined to succeed.

We didn't get a loan during COVID, since the work economy was declining.

Luckily, our owner wanted to sell the condo, so we inquired about using the "Rent to own" option to proceed with the purchase.

Here is how I purchased and paid off a $171,278 property within three years:

- Big Down Payment - I made a big down payment

- Big Monthly Payment - I created a plan of action and a realistic budget

- Big Time Tracking - I kept track of monthly payments each and every month

1. Making A Big Down Payment

You need a down payment, whether you are purchasing or renting.

I made a budget, reduced unnecessary spending, and lived a simple life in order to put enough money together for the down payment.

Although it was difficult, I always reminded myself that the goal was to become a homeowner.

Each time I wanted to buy something, anything, I thought, do I really need this, or do I need a home?

On top of that, I was able to utilize the rental deposit in the downpayment as well as the monthly payment that I paid when the purchase “Rent to own” agreement was signed.

The seller provided a personal financing option so we didn’t have to worry about bank approvals, etc.

I took out personal loans from family and friends in order to cover the biggest downpayment (that was around 28-30%). We agreed on a monthly schedule, so basically we started paying a $2000 rent payment, which was taken as the mortgage payment.

Here is the simple breakdown:

$1400 rent payment - we were paying before we started the rent-to-own contract

$2000 monthly payment - I increased the monthly amount by $600 each month in order to pay the total amount quickly.

The only catch was that I couldn’t miss any payments; if I did, then we would lose everything (house plus down payment).

We agreed to pay the balance on a monthly basis, so we simply started making $2000 payments for rent, which were categorized as mortgage payments.

2. Plan A Big Monthly Payment With A Realistic Budget

I knew that the length of my mortgage would determine the amount of interest I would ultimately pay.

I had to make sure that I had reasonable expectations for both my monthly payments and my yearly one-time payment.

With the rent-to-own agreement in place, I made a payment plan and allocated money in my budget to make extra one-time mortgage payments in order to pay off my mortgage more quickly.

I also began to live even more simple life, reduce superfluous spending, and pay my mortgage with every additional dollar.

Here is a screenshot of how the schedule looked:

3. Tracking Progress Each Month

Paying a big down payment along with monthly payments wasn’t easy, but it was super important to keep track of progress.

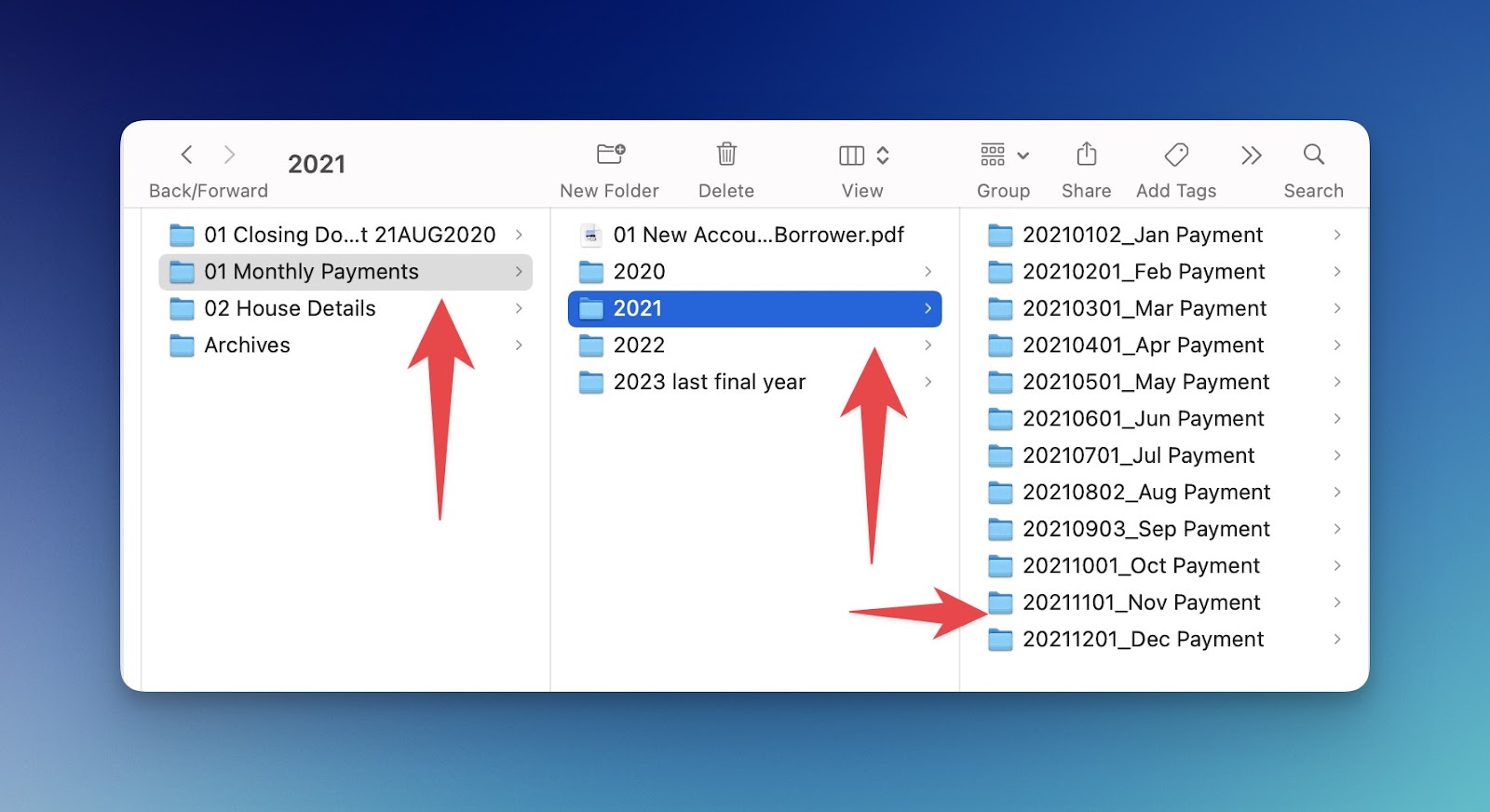

I meticulously organized my payment receipts in monthly folders and documented every transaction in Google Sheets.

Here is a quick screenshot to show you how my folder structure looked:

After three years of steady dedication, I paid off my mortgage in full.

I felt happy and proud of myself for accomplishing my goal of becoming a house owner.

The sense of accomplishment and pride in becoming a homeowner was indescribable—out of this world.

Now, I can focus on improving the value of my house and developing equity because I am no longer concerned about making monthly mortgage payments.

Conclusion

Transitioning from renting to homeownership wasn't easy, but it was undoubtedly worthwhile.

I learned how critical budgeting, saving, and making sacrifices are to achieving my long-term objectives.

Once I've established the long-term, three-year target, I only focus on one day (one month) at a time.

If having your own home is something you've always desired, know that it is practical with dedication, perseverance, and a solid plan.

Don't give up on your goals and what you want to accomplish—take control of your finances and embark on the rewarding journey of homeownership.

Cecilia Cuello: A Remarkable Realtor Who Made It Happen

I’d like to take this opportunity to convey my heartfelt gratitude to the property manager and realtor, Ceclia Cuello, whose unwavering support and assistance made this achievement possible.

Direct Axess

Direct Axess

Cecilia, you are genuinely remarkable, and without your enormous assistance and support, this would not have been possible.

If you're looking for a new home, use the contact link below to reach Cecilia.

Highly recommended!